L E H A V R E

N E W S

7

D E C E M B E R Le Havre Board President Stanley Greenberg sat down recently with Habitat

Magazine to discuss the “ups and downs” of Le Havre’s history, from its development

in the 1950s, to its conversion to a co-op in the 1980s, to its present and future

improvements. Following is a reprint of that article.

The Rollercoaster Ride at Le Havre

Co-op Nears a New Peak

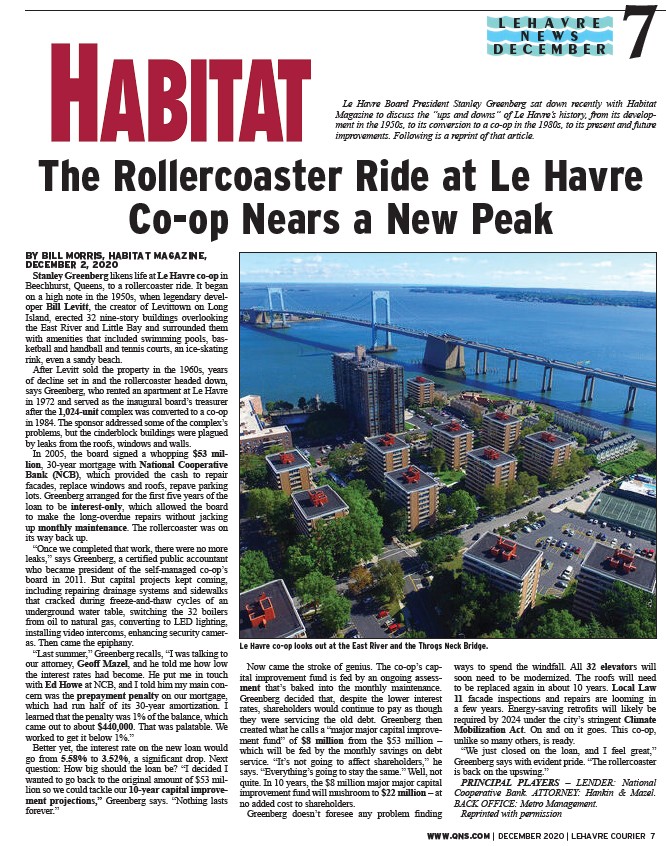

Le Havre co-op looks out at the East River and the Throgs Neck Bridge.

WWW.QNS.COM | DECEMBER 2020 | LEHAVRE COURIER 7

BY BILL MORRIS, HABITAT MAGAZINE,

DECEMBER 2, 2020

Stanley Greenberg likens life at Le Havre co-op in

Beechhurst, Queens, to a rollercoaster ride. It began

on a high note in the 1950s, when legendary developer

Bill Levitt, the creator of Levittown on Long

Island, erected 32 nine-story buildings overlooking

the East River and Little Bay and surrounded them

with amenities that included swimming pools, basketball

and handball and tennis courts, an ice-skating

rink, even a sandy beach.

After Levitt sold the property in the 1960s, years

of decline set in and the rollercoaster headed down,

says Greenberg, who rented an apartment at Le Havre

in 1972 and served as the inaugural board’s treasurer

after the 1,024-unit complex was converted to a co-op

in 1984. The sponsor addressed some of the complex’s

problems, but the cinderblock buildings were plagued

by leaks from the roofs, windows and walls.

In 2005, the board signed a whopping $53 million,

30-year mortgage with National Cooperative

Bank (NCB), which provided the cash to repair

facades, replace windows and roofs, repave parking

lots. Greenberg arranged for the first five years of the

loan to be interest-only, which allowed the board

to make the long-overdue repairs without jacking

up monthly maintenance. The rollercoaster was on

its way back up.

“Once we completed that work, there were no more

leaks,” says Greenberg, a certified public accountant

who became president of the self-managed co-op’s

board in 2011. But capital projects kept coming,

including repairing drainage systems and sidewalks

that cracked during freeze-and-thaw cycles of an

underground water table, switching the 32 boilers

from oil to natural gas, converting to LED lighting,

installing video intercoms, enhancing security cameras.

Then came the epiphany.

“Last summer,” Greenberg recalls, “I was talking to

our attorney, Geoff Mazel, and he told me how low

the interest rates had become. He put me in touch

with Ed Howe at NCB, and I told him my main concern

was the prepayment penalty on our mortgage,

which had run half of its 30-year amortization. I

learned that the penalty was 1% of the balance, which

came out to about $440,000. That was palatable. We

worked to get it below 1%.”

Better yet, the interest rate on the new loan would

go from 5.58% to 3.52%, a significant drop. Next

question: How big should the loan be? “I decided I

wanted to go back to the original amount of $53 million

so we could tackle our 10-year capital improvement

projections,” Greenberg says. “Nothing lasts

forever.”

Now came the stroke of genius. The co-op’s capital

improvement fund is fed by an ongoing assessment

that’s baked into the monthly maintenance.

Greenberg decided that, despite the lower interest

rates, shareholders would continue to pay as though

they were servicing the old debt. Greenberg then

created what he calls a “major major capital improvement

fund” of $8 million from the $53 million –

which will be fed by the monthly savings on debt

service. “It’s not going to affect shareholders,” he

says. “Everything’s going to stay the same.” Well, not

quite. In 10 years, the $8 million major major capital

improvement fund will mushroom to $22 million – at

no added cost to shareholders.

Greenberg doesn’t foresee any problem finding

ways to spend the windfall. All 32 elevators will

soon need to be modernized. The roofs will need

to be replaced again in about 10 years. Local Law

11 facade inspections and repairs are looming in

a few years. Energy-saving retrofits will likely be

required by 2024 under the city’s stringent Climate

Mobilization Act. On and on it goes. This co-op,

unlike so many others, is ready.

“We just closed on the loan, and I feel great,”

Greenberg says with evident pride. “The rollercoaster

is back on the upswing.”

PRINCIPAL PLAYERS – LENDER: National

Cooperative Bank. ATTORNEY: Hankin & Mazel.

BACK OFFICE: Metro Management.

Reprinted with permission

/WWW.QNS.COM